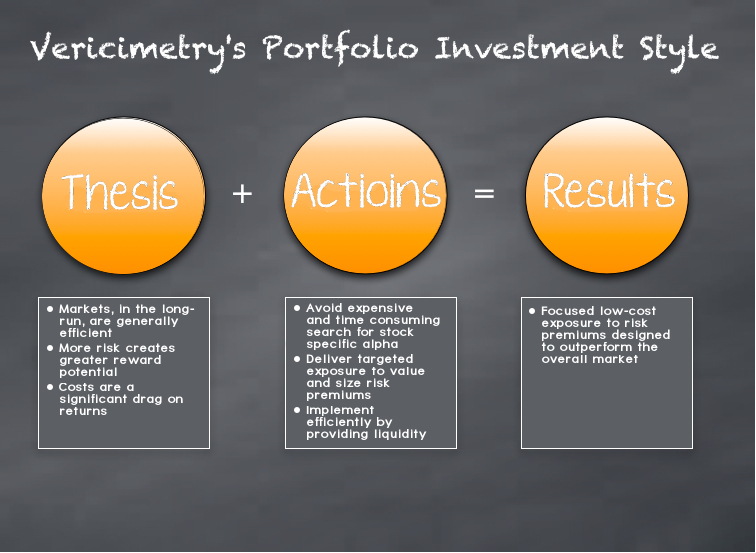

Thesis #1: Markets Are Efficient

The market efficiency concept is that all information about a security is reflected in its price. We believe there is good conceptual and empirical evidence regarding market efficiency. Numerous academic studies have examined mutual fund returns with results consistently showing that active stock picking investment managers have failed to add value after investment manager fees and investment expenses.

Thesis #2: Risk and Reward Are Related

Finance theory suggests that there is a way to beat the market: take more risk. That greater risk leads to greater reward (or greater loss) is a plausible and well known tenet, and one for which substantial empirical evidence exists.

Thesis #3: Relationship Between Costs and Investing

The equity market is the collective sum of the actions of all its participants. When someone profits, another loses by an equivalent amount. Therefore, if equity markets are efficient, on average the returns of a participant are equal to the returns of the equity market minus their collective costs. These costs include management fees, trading costs and taxes.

We find that there is substantial conceptual and empirical evidence to support our three core beliefs. These core beliefs form the basis of our philosophy and thus determine the way we act on behalf of our clients. These actions are to avoid the search for alpha, capture risk premiums and implement in an efficient manner.

Click Image to Enlarge

Click Image to Enlarge